Principled profits: What ESG means for private investors

copied!

copied!

“Ask not what your cash can do for you, but what your cash can do for the world.” A naively optimistic interpretation of private investor motivations, or a realistic acknowledgement of the way the investment wind is blowing?

Increasingly, these dual motivations – to make money while simultaneously doing good – are interconnected. This happy convergence goes some way to explaining the surge over the last decade in ESG (environmental, social and governance) investing – the kind of investing whereby funds are funneled into opportunities with a demonstrable environmental, societal or moral dimension, as certified by an independent third party.

These days, supporting the development of a more sustainable society often runs in tandem with capital growth. It’s not about virtue signaling or scoring social media points by showing off your support for human rights, the environment, diversity and transparency – all frequent ESG touchstones – rather, far-sighted private investors recognize that a secure, stable world is one naturally primed for growth and predictability – two hallmarks of a fertile and secure commercial landscape. In contrast, a world riven with societal stresses and environmental instability, is more often than not, synonymous with volatility, uncertainty and long-term decline – hardly a solid basis for long term economic growth.

In the World Economic Forum (WEF) 2022 Global Risk Report, the leading risks facing the world in terms of likelihood and impact (extreme weather, climate action failure, biodiversity loss, human-made environmental disasters, weapons of mass destruction and water crises[1]) have one thing in common: the chances of their occurrence, and their severity, are determined by the robustness of the world we all share.

The safer the planet, and the more stable the civilization upon it, the more financial opportunities will emerge. So what exactly do we mean by ‘ESG’? There is no single definition, but McKinsey provides a helpful starting point in an article on ESG investing:

The E – environment – reflects the fact that every company uses energy and resources; every company affects, and is affected by, the environment. E includes the energy an organization uses and the waste it discharges, the resources it needs, and the resulting consequences for the planet. It encompasses carbon emissions and climate change.

S – social – recognizes that every company operates within a broader, diverse society. It addresses the relationships a business has and the reputation it fosters with people and institutions in the communities where it operates. S includes labor relations and diversity and inclusion.

G – governance – addresses the issue that every organization, themselves as legal entities, require governance. It refers to the internal system of practices, controls, and procedures a business adopts to govern itself, make effective decisions, comply with the law, and meet the needs of external stakeholders. [2]

The ESG movement has its roots in 2005, when Kofi Annan, the then UN Secretary-General, invited a group of the world’s largest institutional investors to develop the Principles for Responsible Investment (PRI), which centered around tackling the ESG issues. The 521 signatories of the PRI now manage more than US$ 103 trillion (latest complete data as of March 2020) in line with the ESG principles[3].

By its very nature, ESG investment means jettisoning the ‘quick-buck-now’ principles of short-termism. A savvy ESG investor will consider, for example, how an investment today in a sustainable energy operation in the developing world will potentially help foster a nation ripe with commercial possibilities a generation down the line. In its purest, or ideal form, ESG investing merges principles with profit.

And so far, that seems to be a winning pitch.

In fact, a 2019, Harvard Business Review study found that sustainability and environmental, social, and governance issues are now a top priority for leading investment firms and public pension funds.[4] In practice this means the world’s largest asset owners have trillions invested in the global economy and multigenerational obligations that call for a long-term view of systemic risks – so they cannot afford to let the planet fail.

What is sustainable investing?

Sustainable investing encompasses a range of strategies that can be used in combination. Some of the most common ones include:

- Negative/exclusionary screening: eliminating companies in industries or countries deemed objectionable.

- Norms-based screening: eliminating companies that violate some set of norms, such as the Ten Principles of the UN Global Compact.

- Positive/best-in-class screening: selecting companies with especially strong ESG performance.

- Sustainability-themed investing: such as in a fund focused on access to clean water or renewable energy.

- ESG integration: including ESG factors in fundamental analysis.

- Active ownership: engaging deeply with portfolio companies.

- Impact investing: looking for companies that make a positive impact on an ESG issue while still earning a market return.

A multi-trillion-dollar force for good

If money talks, then the voice of ESG investing is coming through loud and clear.

A report by global business advisors Deloitte looking at the growth of ESG over the past few years shows that 70% of responsible investment funds outpaced comparable alternatives in the first quarter of 2021. During that same period, 24 out of 26 sustainable index funds outperformed related conventional index funds. Some 90% of studies, according to Deloitte, reinforce the long-term benefits and relationship between ESG and company financial performance.[5]

This over-performance will only inspire more confidence in the concept of ESG investment.

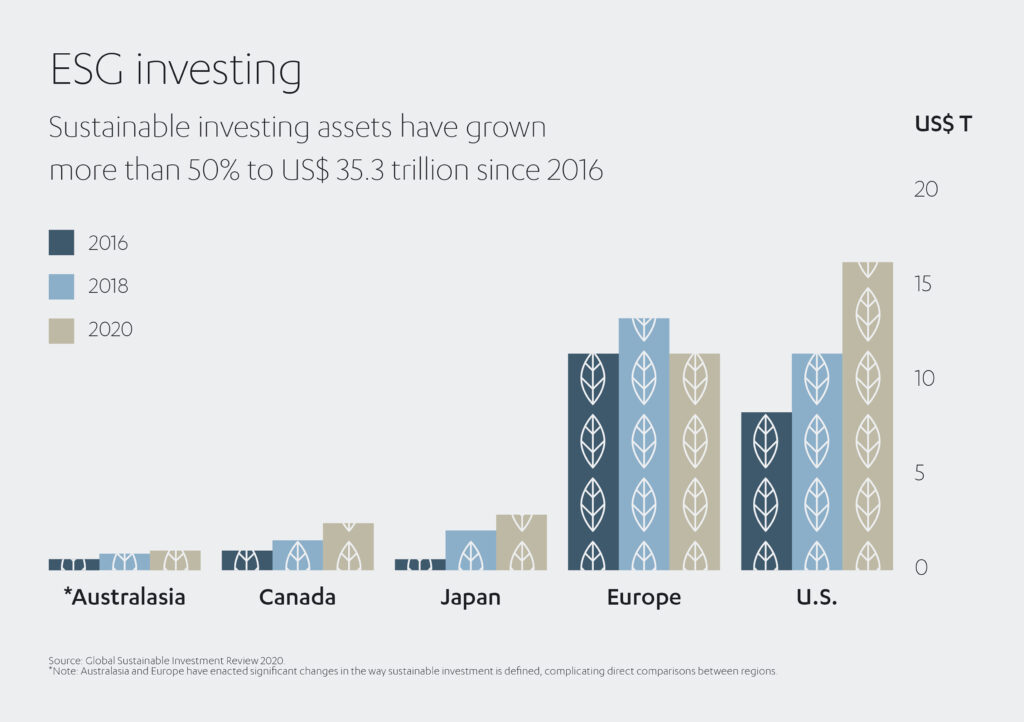

Between 2016 and 2020, sustainable investment assets grew more than 50% to US$ 35 trillion around the world.[6] By 2025, it is estimated that sustainability portfolios and funds globally could hold more than US$ 53 trillion of investments.[7]

Such growth is perhaps unsurprising, given that new research shows the majority of consumers across 17 major markets believe financial services, companies and investors should be doing more to help the environment.[8]

Tackling ‘greenwashing’

Naturally, with greater influence and attention comes greater responsibility, so accountability becomes paramount.

Corporate ESG claims, along with financial products such as green bonds or specialized green exchange traded funds (ETF), are routinely subject to qualitative and quantitative assessment of the ESG related disclosures they make. However, reporting standards still need to improve and standardize to counter some of the criticisms beginning to emerge around the ESG process.

Chief among these is ‘greenwashing’, where an organization makes grand claims about the ESG credentials of its products or policies that cannot be supported by objective, verifiable, metrics. It is a problem which can leave well-intentioned private investors floundering and undermine the wider cause.

The problem of greenwashing is more than just hypothetical. UK-based climate crisis think tank InfluenceMap revealed last year the results of its analysis of 723 ESG-themed funds (worth more than US$ 330 billion in asset value) showing that most failed to align with the Paris Agreement’s long-term goal of limiting temperature rises to below 2 degrees Celsius.[9]

In its 2020, report ‘ESG Investing: Practices, Progress and Challenges’, the Organization for Economic Co-operation and Development (OECD) highlighted key areas for improvement to prevent greenwashing and help unlock the true value of ESG finance.[10] Among them:

- Ensuring consistency, comparability and quality of core metrics in reporting frameworks for ESG disclosure.

- Levelling the playing field between large and small issuers regarding ESG disclosures and ratings.

- Promoting the transparency and comparability of scoring and weighting methodologies among established ESG ratings providers and indices.

- Ensuring clear labelling and disclosure of ESG products, to adequately inform investors of how ESG is used in asset selection.

In response, lawmakers around the world are gradually turning their gaze towards ESG markets to ensure future investment decisions are based on the best information available. Progress, however, varies from region to region.

Private investors gaining greater insight into ESG

Internationally, a patchwork of bodies including the Task Force on Climate-Related Financial Disclosures and the International Organization of Securities Commissions are striving to create a universal disclosure regime.

Momentum is inarguably building behind efforts to harmonize the international ESG investment system.

Last year, for instance, saw the launch of the Net Zero Banking Alliance, a UN-led project uniting more than 50 banks from 24 countries in the quest for net zero emissions. The precedent-setting Network for Greening the Financial System, active since 2017, brings together central banks and regulators with shared climate goals.

The International Financial Reporting Standards Foundation’s (IFRS) new International Sustainability Standards Board is another step in the right direction.

The board aims to ensure reliable and comparable company ESG reports across a key set of consistent metrics, helping private investors large and small find their own sustainable/economic sweet spot with greater clarity.

Efforts are also under way at regional level to improve transparency. The WEF notes in its recent report on sustainable investing that regulators in the UK, US and EU are subjecting green claims and sustainable financial products to closer monitoring.[11]

In the UK, the job of establishing the legitimacy of ESG investments falls principally to the Financial Conduct Authority (FCA). The FCA is involved in the ongoing process of devising a system that must be, as reported in the Financial Times, “straightforward and nuanced, stringent but flexible, endorsed by experts yet clear to consumers.” [12]

In 2021, the FCA published a set of guiding principles for ESG-labelled funds to improve the quality of applications and improve investor faith in the market. The principles cover everything from fund names to investment strategies, to stewardship.

More recently, the FCA has proposed a three-tier disclosure process for prospective investees, comprising a clear product label, consumer-friendly key facts, and a deeper dive for potential investors.[13]

Across the Atlantic, Securities and Exchange Commission (SEC) investigators in the US are requiring fund managers to be more explicit about the classification process for ESG labeling, particularly regarding the trillions of dollars of sustainable assets traded on Wall Street.[14]

In a sign of greater scrutiny to come, the SEC has also demanded fund managers supply further data on ESG compliance covering regulatory filings and promotion.

Already the SEC has flagged-up concerns that some ESG funds could not justify their green claims and exposed a chasm between marketing and reality.[15]

Part of the problem has stemmed from US delays in formalizing official criteria for ESG qualification.

In Europe, the newly unveiled Strategy for Financing the Transition to a Sustainable Economy outlines tighter reporting rules for financial entities and proposes incorporating climate-related risks into credit ratings.[16]

This year the EU will adopt its landmark Corporate Sustainability Reporting Directive (CSRD) replacing the previous Non-Financial Reporting Directive (NFRD). The CSRD compels all large and listed European companies to adopt mandatory sustainability reporting standards and provide external assurance of their ESG performance.[17]

The EU’s Sustainable Finance Package, a cornerstone of the region’s post-COVID economic fightback, includes the EU Taxonomy and Sustainable Finance Disclosure Regulation. The new rulebook aims to clarify some of the existing grey areas in reporting, while simultaneously encouraging investment in environmentally conscious industries.[18]

Crucially, the taxonomy classifies, for the first time, which sectors of the economy can claim to be sustainable investments. Earning a green label means featuring on the list of approved economic activities and meeting a series of detailed environmental criteria.

The system covers three types of investment opportunities:

- Those directly aiding net zero ambitions, such as renewable energy projects.

- Associated necessary infrastructure, such as storage plants.

- Traditional activities unable to turn 100% sustainable but producing below-average emissions and helping with the transition to a green future.

Private funding is considered central to Europe’s target of net zero emissions by 2050, so it is hoped the overhaul will help attract new investors to the marketplace.

The stakes for ESG investing could hardly be higher, with the International Monetary Fund recently spotlighting the significance of private sector finance for government climate legislation worldwide.[19] Mitigating climate change could cost up to US$ 500 billion annually by 2050, a bill government cannot meet alone.

Private investors are among those destined to fill the financing gap and reap the respective rewards. And as the data behind ESG comes into ever sharper focus, investors can begin to fully explore the possibilities presented by the power of ethical finance.

Compiling a healthy ESG portfolio

If ESG is the door to principled profit, then research is the key which unlocks it. ESG as a major investment nexus is still a relatively young concept and exists presently in a state of transition.

For potential private investors, this means rigorous due diligence is required into all the operational, legal and regulatory facets of an opportunity – particularly as the transition to a low-carbon society could itself cause potential logistical and economic disruptions.

Impartially assessing an investment’s exposure to climate risk, for example, can help bolster it against these potential disruptions, while also shining a light on opportunities just over the horizon.

In a world increasingly prone to unforeseen shocks (Brexit, COVID-19, geopolitical conflict) a diversified portfolio is prudent to avoid overexposure to any one particular industry, region, company or investment vehicle. For some experts, the risks of an ESG-weighted portfolio can therefore be reduced by spreading investments across a range of sectors, equities and legislative territories.[20]

In a report on incorporating ESG within investment portfolios, Deloitte suggests a four-step approach to interpreting value throughout an investment life cycle.[21]

- Strategy: Defining core ESG objectives and methods, then establishing metrics for examining opportunities through the lens of ESG priorities.

- Investing activities: Establishing policies to evaluate the ESG performance of target companies and using these outcomes to inform decisions.

- Ownership and reporting: Ensuring investees collaborate on data collection and reporting so ESG performance can be measured against designated metrics; then obtaining independent third-party confirmation of ESG performance.

- Exit: Evaluating the target’s ESG success to date in terms of performance and reporting processes.

For the private investor, a promising opportunity might be one where robust oversight structures are already in place, where ESG is accommodated across a broad investment strategy, and where dependable data illuminates risk and opportunity alike.

Often it is private investors, independent and fast to act, who are in the best position to capitalize on these shifting opportunities within ESG.

Aside from portfolio diversification, keeping abreast of current affairs and being market savvy pays dividends: as an investor operating in the still-evolving world of ESG, it can help to anticipate future political and economic trajectories. A global perspective is likewise important, because sustainable investing can look very different from region to region. Research should always be industry-specific because the boundaries of ‘risk’ can vary considerably from sector to sector – the climate risks of agriculture require a different approach to the reputational risks of retail, for instance.

Many ESG investors focus on nimble companies within industries best primed to grow in value as they increasingly embrace sustainability. ESG patterns are still emerging, so the most successful private investors may well be those who prioritize long-term returns and exercise caution towards unsustainably high short-term yields.

How best to ensure your money is making a difference? Be wary of headline ESG claims, because companies might only want to share good news. Look deeper. Rely on different ratings systems, such as Moody’s Sustainalytics, MSCI, S&P Global, and ensure you can verify the source of any data used. Exploit the possibilities of shareholder resolutions and proxy votes to encourage more diverse boards and greater disclosure on environmental impacts. And finally, ask what issues most matter to you.

Free from the indecision of corporate boards and the whims of shareholders, private investors are ideally placed to make their own decisions and set their own benchmarks for determining success.

Private capital is patient capital – it doesn’t need to deliver a deliver a short-termist blockbuster quarterly return, but can instead ride out the ripples of our changing world and deliver steady, long term results.

Leading by example

Channeling private capital into climate change action is a core aim of the JIMCO Strategic Asset Fund, operated by the Jameel Investment Management Company (JIMCO).

Since 2018, the Fund has injected capital into funds that support sustainable opportunities worldwide, including funds that are building sustainable portfolios around resource efficiency, decarbonization, renewables, distributed energy, electrification, mobility and water infrastructure.

One such fund invests in sustainable farming in New Zealand.

It deploys innovative technology and business models to introduce a ‘regenerative’ approach to food production, effectively reversing the damage to water, soil, climate and biodiversity systems caused by agriculture.

Altogether, the JIMCO Strategic Asset Fund has committed around US$ 2.5 billion of investment to more than 65 funds globally – an exciting first chapter in what is set to become a decades-spanning mission.

JIMCO has also made significant investments in more sustainable mobility startups.

Take US-based Rivian, which develops electric vehicles and sustainable services solutions. Rivian is producing an electric SUV and pickup truck, and in parallel with this is planning an extensive charging network throughout North America. The company’s IPO on the Nasdaq exchange in November last year raised almost US$ 12 billion for a valuation of US$ 66.5 billion.[22]

Turning to the skies, JIMCO has also invested in California-based Joby Aviation, currently developing an electric vertical take-off and landing aircraft for air taxi services.

Its second prototype aircraft is currently undergoing testing at the company’s production headquarters, ahead of a possible 2024 service start date.

“The numbers are hard to debate – private equity has vast potential to help the world meet its ambitious climate goals and help foster a fairer, safer society for all,” says Sidhesh Kaul, Chief Executive Officer, JIMCO and VP Investments for Abdul Latif Jameel.

“Giant strides are being made in improving reporting standards across ESG opportunities, meaning potential investors can place greater faith then ever in ESG claims backed by empirical data.

“Inevitably more needs to be done to unify measurable criteria internationally. However, we are only just witnessing the beginning of a multi-trillion-dollar investment market, one which uniquely straddles both the economic and ethical spheres.”

[1] https://www3.weforum.org/docs/WEF_Global_Risk_Report_2020.pdf

[2] https://www.mckinsey.com/business-functions/strategy-and-corporate-finance/our-insights/five-ways-that-esg-creates-value

[3] https://www.valueresearchonline.com/stories/49015/the-rise-of-esg-investing/

[4] https://hbr.org/2019/05/the-investor-revolution

[5] https://www2.deloitte.com/content/dam/Deloitte/us/Documents/audit/us-audit-incorporating-esg-across-investment-portfolios-may-open-access-to-capital.pdf

[6] https://www.bloomberg.com/news/articles/2021-09-03/fund-managers-feel-heat-in-sec-crackdown-of-overblown-esg-labels

[7] https://www.bloomberg.com/professional/blog/esg-assets-may-hit-53-trillion-by-2025-a-third-of-global-aum/

[8] https://yougov.co.uk/topics/economy/articles-reports/2021/01/28/should-financial-services-companies-fight-climate-

[9] https://influencemap.org/pressrelease/The-truth-about-climate-funds-most-are-misaligned-with-the-Paris-Agreement-ee40c9b124666a5bee363fea134e3c37

[10] https://www.oecd.org/finance/ESG-Investing-Practices-Progress-Challenges.pdf

[11] https://www.weforum.org/agenda/2021/12/esg-sustainable-investment-backlash/

[12] https://www.ftadviser.com/investments/2022/01/27/can-the-fca-tackle-greenwashing/

[13] https://www.fca.org.uk/publication/policy/ps21-24.pdf

[14] https://www.bloomberg.com/news/articles/2021-09-03/fund-managers-feel-heat-in-sec-crackdown-of-overblown-esg-labels

[15] https://www.sec.gov/files/esg-risk-alert.pdf?utm_medium=email&utm_source=govdelivery

[16] https://www.bloomberg.com/news/articles/2021-06-30/eu-targets-greenwashing-by-financial-sector-in-strategy-draft

[17] https://www.ey.com/en_no/assurance/how-the-eu-s-new-sustainability-directive-will-be-a-game-changer

[18] https://www.reuters.com/business/sustainable-business/what-is-eus-sustainable-finance-taxonomy-2022-02-03/#:~:text=The%20EU%20taxonomy%20is%20a,to%20earn%20a%20green%20label.

[19] https://www.imf.org/Publications/fandd/issues/2021/09/valerie-smith-citi-private-sector-climate-change

[20] https://www.ftadviser.com/investments/2021/04/29/understanding-risk-and-reward-in-an-esg-portfolio/

[21] https://www2.deloitte.com/content/dam/Deloitte/us/Documents/audit/us-audit-incorporating-esg-across-investment-portfolios-may-open-access-to-capital.pdf

[22] https://www.cityindex.co.uk/market-analysis/rivian-ipo-everything-you-need-to-know-about-rivian/

Related Insights